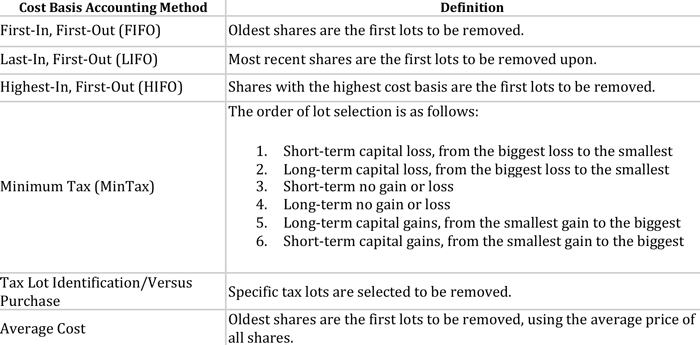

0

items

$0

Investor Basics: Intro to Fundamental Analysis

Contributed by: Nicholas Boguth

There are two major types of analysis when it comes to investing: Technical Analysis, which you can read more about in Angela Palacios', CFP®, Investor PhD blog, and Fundamental Analysis, which I will break down for you right now.

Ultimately, fundamental analysis is an evaluation of the financial position and performance of a company or strategy.

When doing fundamental analysis on a stock, the process involves breaking down all of the quantitative information found on the company’s financial statements. Digging into a company’s balance sheet tells you about their current position as it pertains to assets, liabilities, and shareholders’ equity. The information on income statements and statements of cash flow reveals how the company has performed, or how much expense, revenue, or profit it generated. Fundamental analysis also involves looking at qualitative factors such as management, the business model, accounting practices, and competitors. All of this data is then analyzed, compared to peers, and used to make an investment decision.

The graphic above lays out The Center’s investment selection process. You will see that there is both quantitative and qualitative fundamental analysis done when choosing the strategies in our model. The process is slightly different when comparing all strategies as opposed to only stocks, but the same considerations have to be taken into account before making an investment decision. We look at quantitative factors such as manager tenure, ownership, costs, risk metrics, and return metrics, just to name a few. We also look at a vast amount of qualitative information about the fund companies, managers, and investment team. Fundamental analysis is step one to selecting each individual strategy for our portfolios. If you have questions on how we build portfolios or fundamental analysis, please reach out to our investment team!

Nicholas Boguth is an Investment Research Associate at Center for Financial Planning, Inc.® and an Investment Representative with Raymond James Financial Services.

The information contained in this blog does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Nick Boguth and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Every investor's situation is unique and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation.