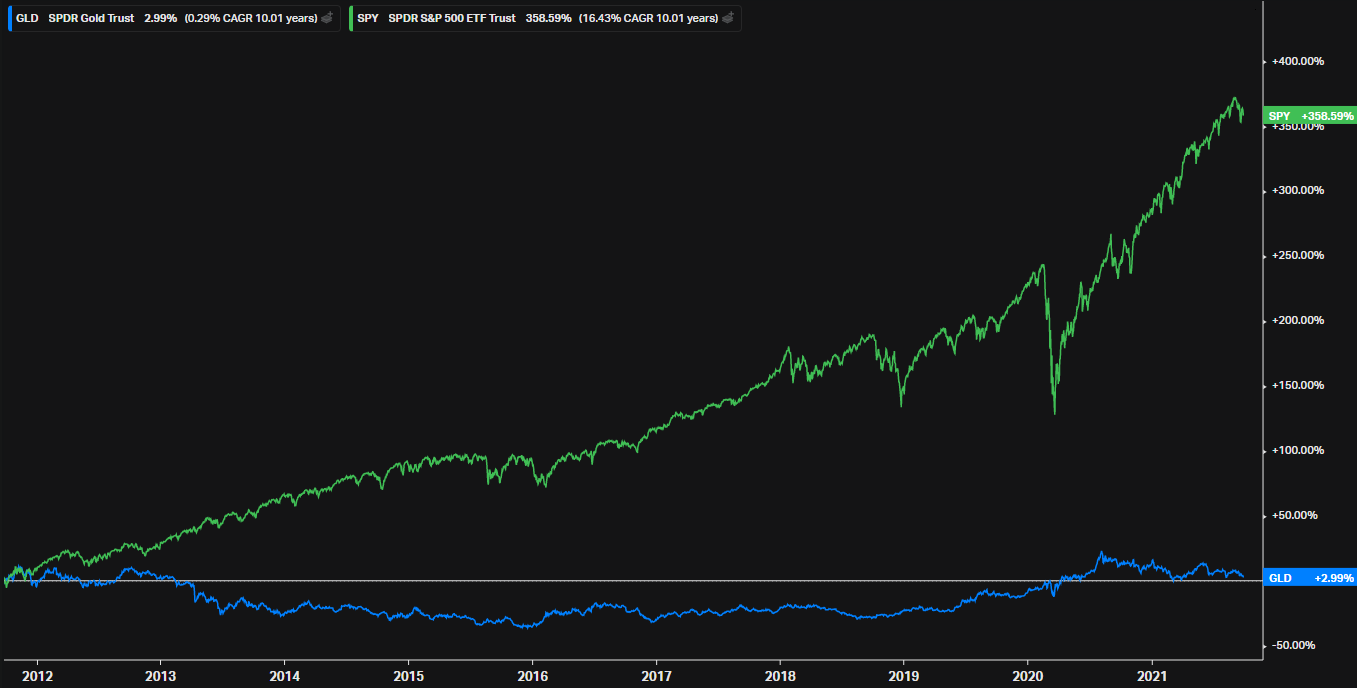

0

items

$0

What to Expect Going Forward - The Economy and Your Investments

Contributed by: Nicholas Boguth, CFA®

Contributed by: Nicholas Boguth, CFA®

At the beginning of the month, RJ released some market commentary with the striking line…

"While inflation fears remain high, it is likely that we are past peak inflation and the largest interest rate increases are behind us."

This year has been riddled with reasons to worry about the economy and your investments, but some encouraging data has been released that may provide some optimism. Jobs surprised on the upside early in August, the stock market has bounced off of its lows, personal consumption remains high, and we've seen gas prices come down to provide relief at the pumps.

RJ ends the commentary with some more encouragement…

"We likely have more weakness to endure, but Joey Madere, senior portfolio strategist, Equity Portfolio & Technical Strategy, says investors can expect positive returns over the next 12 months and beyond, given the view that economic weakness should be relatively mild and inflation will moderate. Long-term investors should anticipate an eventual rally on the other side of this weak trend and take advantage of potential buying opportunities. Bear markets go down 20% to 35% on average, but bull markets average roughly 150% returns.

While volatility feels uncomfortable, experience suggests that adaptability and a cool head will help weather any market environment and position for the future.”

It's been a rough year for most asset classes YTD. Still, the pain and uncertainty also provide opportunity as bond yields increase and stock valuations decrease, suggesting higher expected returns going forward. We're continually monitoring the changing environment and are happy to answer any questions you may have about how it all affects or doesn't affect your overall financial plan.

Nicholas Boguth, CFA® is a Portfolio Manager at Center for Financial Planning, Inc.® He performs investment research and assists with the management of client portfolios.

This market commentary is provided for information purposes only and is not a complete description of the securities, markets, or developments referred to in this material. Any opinions are those of Nick Boguth, CFA® and not necessarily those of Raymond James. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance does not guarantee future results. Diversification and asset allocation do not ensure a profit or protect against a loss.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC. Investment advisory services are offered through Center for Financial Planning, Inc. Center for Financial Planning, Inc. is not a registered broker/dealer and is independent of Raymond James Financial Services.