0

items

$0

Finding the Right Asset Allocation

Contributed by: Jaclyn Jackson, CAP®

Contributed by: Jaclyn Jackson, CAP®

**Register for our LIVE investment event or our investment WEBINAR on Feb. 23!

Most delicious meals start with a great recipe. A recipe tells you what ingredients are needed to make the meal and, importantly, how much of each ingredient is needed to make the meal taste good. Just like we need to know the right mix of ingredients for a tasty meal, we also need to know the asset allocation mix that makes our investment journey palatable.

Determining the Right Mix

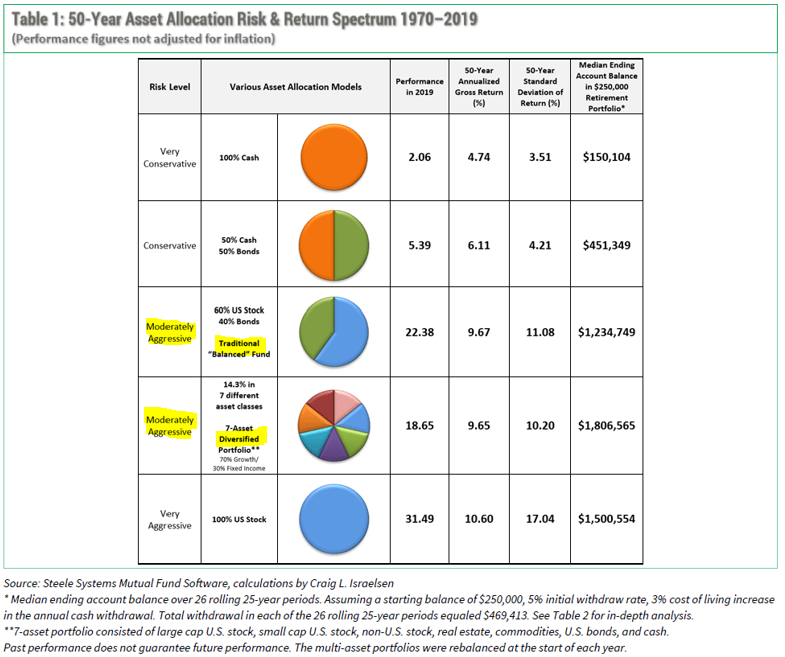

Asset allocation is considered one of the most impactful factors in meeting investment goals. It is the foundational mix of asset classes (stocks, bonds, cash, and cash alternatives) used to structure your investment plan; your investment recipe. There are many ways to determine your asset allocation. Asking the following questions will help:

What are my financial goals?

When do I need to achieve my financial goals?

How much money will I be investing now or over time to facilitate my financial goals?

Seasoning to Taste

Now, suppose equity markets were down 20%, and your portfolio was suffering. Would you be tempted to sell your stock positions and purchase bonds instead? Figuring out an asset allocation based on goals, time horizons, and resources is essential but means nothing if you can’t stick with it. A recipe may instruct us to “season to taste” for certain ingredients. In other words, some things are subjective, and our feelings greatly influence whether we have a negative or positive experience. For asset allocation, understanding your risk tolerance helps uncover personal attitudes about your investment strategy during challenging market scenarios. It gives insight into your ability or willingness to lose some or all of your investment in exchange for greater potential returns. When deciding our risks tolerances, we must understand the following:

The risks and rewards associated with the investment tools we use.

How we deal with stress, loss, or unforeseen outcomes

The risks associated with investing

Following the Recipe

When we follow a recipe closely, our meal usually turns out how we expected. In the same way, committing to your asset allocation increases the likelihood of meeting your investment goals. Understanding your risk tolerances can reveal tendencies to undermine your asset allocation (i.e., selling or buying asset classes when we should not). Fortunately, there are a few strategies you can employ to help stay on track.

If you are risk-averse, diversifying your investments between and among asset categories can help improve your returns for the levels of risks taken.

If you find yourself buying or selling assets at the wrong time, routinely (annually, quarterly, or semi-annually) rebalancing your portfolio will force you to trim from the asset classes that have performed well in the past and purchase investments that have the potential to perform well in the future.

If you find yourself chasing performance or buying investments when they are expensive, buying investments at a fixed dollar amount over a scheduled time frame, dollar cost averaging, can help you to purchase more shares of an investment when it is down relative to other assets (prices are low) and less shares when it is up relative to other assets (more expensive). Ultimately, this can lower your average share cost over time.

Finding the right asset allocation for you is one of the most important aspects of developing your investment plan. Luckily, understanding investment goals, time horizons, resources, and risk tolerances can help you mix the best recipe of asset categories to make your investment journey deliciously successful.

Jaclyn Jackson, CAP® is a Senior Portfolio Manager at Center for Financial Planning, Inc.® She manages client portfolios and performs investment research.

This information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Any opinions are those of Center for Financial Planning, Inc., and are not necessarily those of RJFS or Raymond James. Every investor’s situation is unique and you should consider your investment goals, risk tolerance and time horizon before making any investment or investment decision. Investing involves risk, investors may incur a profit or loss regardless of strategy or strategies employed. Asset allocation and diversification do not ensure a profit or guarantee against a loss. Dollar-cost averaging does not ensure a profit or protect against loss, investors should consider their financial ability to continue purchases through periods of low price levels.