October is Financial Planning Month and Center Partner Tim Wyman takes this opportunity to bring us back to the basics. In this blog 5-part series he clarifies some general questions about financial planning and the financial planning process.

Ok, figuring out financial planning may not be as deep as asking “what is the meaning of life”, but I would assert that pondering both can potentially be life changing. According to the Financial Planning Association®: Financial planning is the long-term process of wisely managing your finances so you can achieve your goals and dreams, while at the same time negotiating the financial barriers that inevitably arise in every stage of life. Remember, financial planning is a process, not a product. Before we get too far, let’s be sure to acknowledge that financial planning is not about get-rich schemes or simply betting on the latest stock tip.

Funding Life’s Goals

As an early leader in the financial planning profession, we at Center for Financial Planning view and practice financial planning in a different manner than many. Financial planning is all about you – your goals – your family – your financial independence. For most, money is not the end but merely the means. Many of life’s goals [sending kids and grandkids to college, funding retirement, starting a business, passing values and asset values to the next generation, etc.] do indeed have a money or financial aspect. So it is critical that you make good financial decisions. Financial planning provides direction, discipline and structure to improve financial decision-making and, dare I suggest, has the power to improve lives.

A Coordinated & Comprehensive Approach

Years ago I was an adjunct professor at Oakland University. On the first day of class, I always started with the assertion, “Financial Planning provides a coordinated and comprehensive approach to achieving your goals,” (it was always question one on the first quiz, by the way). If a coordinated and comprehensive approach is not taken, you are simply left with a junk drawer of decisions and purchases. Without a comprehensive and coordinated strategy, people buy some insurance … put it in the drawer, buy a mutual fund or stock … put it in the drawer … have a living trust drafted … put it in the drawer. Over the years, the individual pieces don’t actually fit together and all that is left is a drawer of stuff (that’s usually impossible to sort through as well).

Integrating Goals with Approach

The financial planning process integrates or coordinates your resources (assets and income) with your goals and objectives. As you do this, here are some key points you should cover:

Goal identification and clarification

Developing your Net Worth Statement

Preparing cash flow estimates

Analysis of income tax returns and strategies designed to help decrease tax liability

Review of risk management areas such as life insurance, disability, long term care, and property & casualty insurance.

College funding goals for children or grandchildren.

Comprehensive investment management and ongoing monitoring of investments

Financial independence and retirement income analysis

Estate and charitable giving strategies

In my next blog, we’ll delve into the difference between wealth management and financial planning. Then we’ll take a closer look at a financial plan, who needs one, and how much you can expect to pay for it.

Timothy Wyman, CFP®, JD is the Managing Partner and Financial Planner at Center for Financial Planning, Inc. and is a frequent contributor to national media including appearances on Good Morning America Weekend Edition and WDIV Channel 4 News and published articles including Forbes and The Wall Street Journal. A leader in his profession, Tim served on the National Board of Directors for the 28,000 member Financial Planning Association™ (FPA®), trained and mentored hundreds of CFP® practitioners and is a frequent speaker to organizations and businesses on various financial planning topics.

Any opinions are those of Center for Financial Planning, Inc., and not necessarily those of RJFS or Raymond James. Every investor’s situation is unique and you should consider your investment goals, risk tolerance and time horizon before making any investment. Clients should evaluate if an asset-based fee is appropriate in servicing their needs. A list of additional considerations, as well as the fee schedule, is available in the firm’s Form ADV Part II as well as in the client agreement.

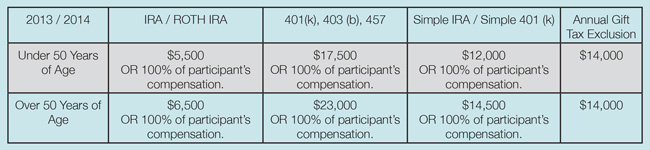

As we approach year-end (yes, already!), it is time to determine what needs to be done to reach your 2013 financial goals AND start preparing for 2014. The 2014 Contribution and Annual Gifting Limits were recently released, and they remain unchanged from 2013 limits. Here is summary of the existing limits for your reference.

As we approach year-end (yes, already!), it is time to determine what needs to be done to reach your 2013 financial goals AND start preparing for 2014. The 2014 Contribution and Annual Gifting Limits were recently released, and they remain unchanged from 2013 limits. Here is summary of the existing limits for your reference.