Contributed by: Nick Defenthaler, CFP®, RICP®

Contributed by: Nick Defenthaler, CFP®, RICP®

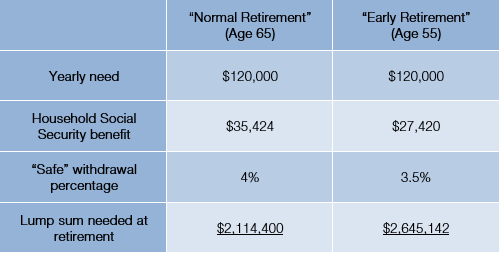

'4% rule' history

In 1994, financial advisor and academic William Bengen published one of the most popular and widely cited research papers titled: 'Determining Withdrawal Rates Using Historical Data' published in the Journal of Financial Planning. Through extensive research, Bengen found that retirees could safely spend about 4% of their retirement savings in the first year of retirement. In future years, they could adjust those distributions with inflation and maintain a high probability of never running out of money, assuming a 30-year retirement time frame. In his study, the assumed portfolio composition for a retiree was a conservative 50% stock (S&P 500) and 50% in bonds (intermediate term Treasuries).

Is the 4% rule still relevant today?

Over the past several years, more and more consumer and industry publications have written articles stating 'the 4% rule could be dead' and that a lower distribution rate closer to 3% is now appropriate. In 2021, Morningstar published a research paper calling the 4% rule no longer feasible and proposing a 3.3% withdrawal rate. Just over 12 months later, the same researchers updated the study and withdrawal rate to 3.8%!

When I read these articles and studies, I was surprised that none of them referenced what I consider critically important statistics from Bengen's 4% rule that should highlight how conservative it truly is:

96% of the time, clients who took out 4% of their portfolio each year (adjusted annually by inflation) over 30 years passed away with a portfolio balance that exceeded the value of their portfolio in the first year of retirement.

Ex. A couple with a $1,000,000 portfolio who adhered to the 4% rule over 30 years had a 96% chance of passing away with a portfolio value of over $1,000,000!

A client had a 50% chance of passing away with a portfolio value 1.6X the value of their portfolio in the first year of retirement.

Ex. A couple with a $1,000,000 portfolio who adhered to the 4% rule over 30 years (adjusted annually by inflation) had a 50% chance of passing away with a portfolio value of over $1,600,000!

We must remember that the 4% rule was developed by looking at the worst possible time frame for someone to retire (October of 1968 – a perfect storm for a terrible stock market and high inflation). As more articles and studies questioned if the 4% rule was still relevant today, considering current equity valuations, bond yields, and inflation, William Bengen was compelled to address this. Through additional diversification, Bengen now believes the appropriate withdrawal rate is actually between 4.5% - 4.7% – nearly 15% higher than his original rule of thumb!

Applying the 4% rule

My continued takeaway with the 4% rule is that it is a great starting place when guiding clients through an appropriate retirement income strategy. Factors such as health status, life expectancy, evolving spending goals in retirement, etc., all play a vital role in how much an individual or family can draw from their portfolio now and in the future. As I always say – there are no black and white answers in financial planning; your story is unique, and so is your financial plan! In my next blog, I'll touch on other considerations I believe are important to your portfolio withdrawal strategy – stay tuned!

Nick Defenthaler, CFP®, RICP®, is a Partner and CERTIFIED FINANCIAL PLANNER™ professional at Center for Financial Planning, Inc.® Nick specializes in tax-efficient retirement income and distribution planning for clients and serves as a trusted source for local and national media publications, including WXYZ, PBS, CNBC, MSN Money, Financial Planning Magazine and OnWallStreet.com.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC. Center for Financial Planning, Inc is not a registered broker/dealer and is independent of Raymond James Financial Services Investment advisory services are offered through Center for Financial Planning, Inc.

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Any opinions are those of Nick Defenthaler, CFP®, RICP® and not necessarily those of Raymond James. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

One cannot invest directly in an index. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. Past performance does not guarantee future results.